Debt, Inflation, and Shortages

"You either have abundance of money and scarcity of everything else, or scarcity of money and abundance of everything else."

- Jeff Booth

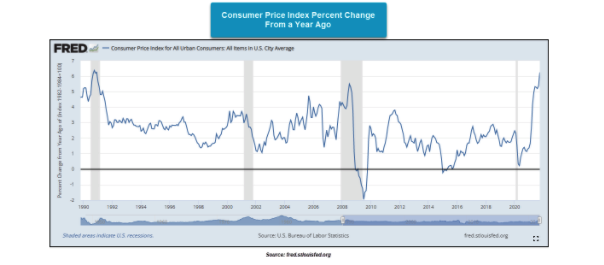

Inflation continues to be one of the biggest stories in the financial world as well as our everyday lives. There is a lot of genuine concern right now about asset price inflation and what it is doing to everyone’s bottom line. On November 10th, the Bureau of Labor Statistics reported inflation rose in October by 0.9%, ahead of expectations of 0.6%. The bureau also reported that year over year inflation rose by 6.2%. This means the US has experienced the largest surge of inflation in 30 years.i 6.2% is a big number and essentially means that $100k sitting in cash for the last 12 months, lost $6,200 of purchasing power. While many people may not be sitting on cash, they are often living on fixed incomes, whether it be ordinary income, pensions, or social security. This type of inflation is very difficult for ordinary people to budget for and it is becoming not only a hot button issue on main street, but now in Washington D.C. as well. The last time the US had inflation readings this high was back in August of 1991 when the Gulf War was going on, and a sharp increase in oil was driving inflation. This is demonstrated in the chart below. In this letter, I will dive into what some of the causes of inflation are, whether or not it is temporary, and how to best protect your portfolio in this environment.

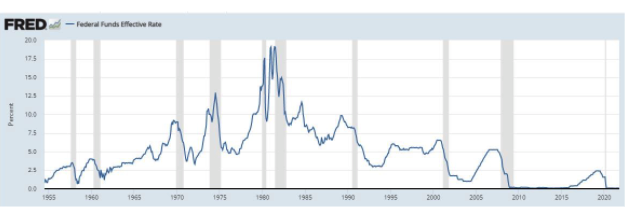

While 6.2% annual inflation may seem high to us, the Fed doesn’t seem overly concerned and appear hesitant to engage in policy to slow inflation. In 2020, the Fed started buying $120 billion of government bonds every month in order to boost the economy. This has largely worked and most of the economy is back to pre-pandemic levels. The long-term objective of the Federal Reserve is a steady 2% inflation and steady employment. Recently, they have overshot their 2% inflation rate but the Fed argue that it was below 2% for a long time and we are now “averaging out.” The Fed is certainly aware of the high inflation and the difficulties it creates for many and have started to slowly make small policy changes that will hopefully ease the inflation for many Americans. In the beginning of November, the Fed announced they would be reducing their bond purchase program by $15 billion per month.ii This policy of buying government bonds every month is inflationary as it expands the monetary supply. While The Fed will continue to purchase around $105 Billion in bonds a month, it is a step towards a more dovish monetary policy. Federal Reserve President James Bullard has also indicated that the Fed will look to raise rates sometime in 2022. As you can see in the chart below, the Federal Funds rate is at 0 and has been close to or at 0 since the great financial crisis in 2010.

When it comes to managing debt and inflation, the Federal Reserve is currently stuck between a rock and a hard place. If inflation continues to run hot, they will need to raise interest rates and drastically reduce/stop buying governments bonds. However, most economists agree that this would greatly slow the economy and could potentially cause the stock market to drop. Not only would these actions be problematic for the economy, they would also be difficult for politicians. The US debt is currently a little over $28 Trillion. In order for Congress to spend money on infrastructure, social spending programs, as well as everyday functions of government, they need the Federal Reserve to buy their debt. The Federal Reserve “prints” money and then uses that “printed” money to buy Treasury Bonds. This is what currently funds, the government, as well as taxes, and it would not be politically feasible to just cut it off. So while the price of food, energy, and almost everything else seems to be going up, it is politically easier to deal with than cutting off spending in Washington.

This may sound like doom and gloom, but it is not. There are signs that inflation is slowing down. A large driver of inflation has been shortages in the automotive sector and manufacturing Anyone who has looked to purchase a car lately knows what I’m talking about. Right now, we currently have a shortage in supply, and large amounts of demand due to high savings and liquidity. Basic economics say that low supply and high demand means higher prices. Recently, automobile and other manufacturer have ramped up output. This could lead to easing inflation going forward. According to the Federal Reserve, industrial production data for October rose 1.6%, well above the expectation for an increase of 0.9%. At the same time, manufacturing output rose 1.2% compared with the expectation for a 0.9% gain. This data points to strengthening supply and hopefully eases some of the bottlenecks and shortages we have been experiencing.

In an inflationary environment, one of the best investment strategies is to own assets or “stuff.” Inflation is simply an expansion of the money supply. When there is more money chasing the same amount of goods, those goods will go up in price. Above and to the left you will see to graphs showing where the strength and weakness are in the market today. On the left, you will see domestic equities and commodities as the strongest and second strongest asset classes. These are what we call “risk on” assets and do well when the market is in an overall uptrend. On the bottom, you see cash and foreign currencies, which we call “risk off.” With inflation not only strong here in the United States, but across the globe, owning currency and cash is a guaranteed losing proposition. Remember, inflation in the US means cash is losing 6.2% of it’s value a year right now. This also leaves fixed income near the bottom. With interest rates still being low, and much lower than the rate of inflation, fixed income has been viewed as less attractive. Historically, a 60/40 portfolio of 60% equities and 40% bonds has been the benchmark. With many bonds yielding much less than inflation, investors are questioning the benefit having that large a percentage of a negative yielding asset.

As far as commodities are concerned, it should come as a surprise to see energy and industrial metals as the strongest in this asset class. In the past 12 months the demand for oil has dramatically increased and we are feeling the pain at the pump. Likewise, industrial metals have been strong over the past 12 months due to a combination of increased manufacturing and money supply. Another tailwind for commodities has been the “green revolution.” Elements like, lithium and cobalt are vital for solar panels and electric vehicles. I also like Uranium as nuclear energy is being viewed as the most efficient way to reduce the global carbon footprint in the foreseeable future.

2021 has been a great year for the stock market as many of the indexes are at or near all-time highs. This has been pleasing for me and my clients as account values have been steadily increasing. The market performance has been great but it also needs to be looked at in real terms as well. Inflation has certainly been a big driver of the market increase and needs to be discounted against gains. Almost all markets have been going crazy as many people are more flush with cash than they have been in the last 10 years. The question on everyone’s mind is how long can this last? While I have no idea how long this bull market can continue or how high it will go, one thing I can say is that the market tends to be irrational longer than you can stay solvent. Meaning it is not in your best interest to time the market or short stocks.

At the end of my last market commentary a couple months ago I said, “interest rates should stay low, inflation will remain above average, and we should have higher than average stock market returns.” This is exactly what happened. I believe the Fed will continue to keep rates at zero and will look for any reason not to raise them. I also think the Fed will continue their bond buying program and will continue look for any excuse not to taper. While inflation may hurt savers and those living on a fixed income, our government needs to spend money in order to stay operational.

In the meantime, I will continue to keep a close on accounts and will be scanning the market for opportunities and threats. A few things I am keeping an eye on is the Democrats social spending bill. There have been rumors that they may eliminate the backdoor Roth conversion for higher earners. I am also hearing there may be an increase in the State and Local Tax deduction (SALT). This would be a big tax break for higher earners and something I will keep a close eye on. It is all unknown for now, but once the details are finalized, I will cover them in my next letter.

Happy Thanksgiving!

Sincerely,

Bruce Carlson, CFP®

President

Carlson Asset Management